.webp)

Reviewing Four P2P Lending Platforms: Our Personal Experience

- J+A

- 15 jul 2025

- 6 minuten om te lezen

More and more people are discovering Peer-to-Peer (P2P) lending as an alternative way to grow their money. There are many options for crowdfunding businesses, but also for private individuals. Interest rates on savings accounts remain very low, making alternatives like P2P still attractive. P2P platforms are also very accessible for beginners: you can often start with as little as €10, without having to deal with fees or other costs.

We ourselves started with P2P lending around 2017/2018 — a period during which various platforms emerged and this way of investing received more attention.

In this blog, we share our personal experiences with four well-known P2P platforms: Bondora, Twino, Mintos, and Robocash. Important to note: this is not financial advice. Everyone should make their own investment decisions based on individual research, goals, and risk tolerance. No tool, platform, or investment will make you rich overnight.

Platforms We Personally Tested:

What is Peer-to-Peer Lending?

In short: with P2P lending, you lend money to others through an online platform, usually in exchange for interest. The platforms connect investors and borrowers. Each platform has its own terms, risk levels, and returns.

Our Experience Per P2P lending Platform

Robocash

Average Return

Robocash is a slightly older P2P lending platform offering peer-to-peer loans. It launched in 2016, focusing on

short-term consumer loans and a fully automated investment approach. It’s popular due to its hands-off strategy and buyback guarantee, which minimizes default risk.

Originally focused on Europe and Russia, it has increasingly shifted toward Asian markets in recent years (Philippines, Kazakhstan, India). This offers new opportunities but also introduces different risks.

Pros:

Fully automated, ideal for passive investing without manual selection

High and consistent returns of 10–12% per year

Buyback guarantee on all loans: buyback after 30–60 days of default

No currency risks or hidden fees; investing in euros

Low entry threshold from €10

Cons:

Limited transparency about Robocash’s and its lenders' financial health

No secondary market; funds are tied up until loans mature

Limited control over individual loans or risk profiles

Focus on Asia brings political and credit risks

Total earned interest (& in 2024)

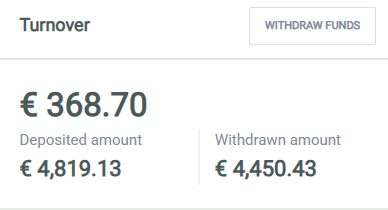

Our Experience – Then and Now

We were involved from the beginning and were among the first 1,000 investors. It’s currently the only

platform we still invest in. Returns have been stable around 10–11%, perfect for passive, reliable income. Automation and the buyback guarantee provide low maintenance and relatively low risk.

We had a period where we had more money invested, but never a huge amount (as seen in the images).Given the stable returns, we leave the money on the platform and occasionally deposit more when we have excess cash.

Bondora

Bondora was the first p2p lending platform we invested in, and it immediately stood out for its ease of use. Since launching Go & Grow in 2018, Bondora has positioned itself as an entry-level product that lets you grow your money automatically at a fixed return, with daily withdrawals.

Pros:

Go & Grow: simple, automated option with fast access to your money, withdrawable 24/7 through controlled procedures

Fixed interest up to 6% per year: since April 1, 2025, a uniform 6% rate applies across the entire Go & Grow balance, no tiered rates or limits

Long track record: active since 2009, with millions in investments, which builds trust

User-friendly: suitable for beginners, with automatic diversification across European loans and a transparent dashboard

Cons:

Return limited to around 6%, lower than riskier categories and some alternative platforms

No buyback guarantee: default risk lies with the investor

Liquidity risk: although daily withdrawals are possible, during stressful periods (like COVID-19), withdrawals may be delayed

Limited secondary market for Portfolio Manager/Pro; Go & Grow mainly offers its own liquidity

Platform risk: Bondora operates without a banking license or deposit guarantee, so your capital isn’t protected by official insurance

Data & Figures

Interest rate cut in 2025: from 6.75% to 6% under uniform conditions

Strong user and volume growth: over €26 million in new Go & Grow investments per month and record returns of €3.16 million in March 2025

Risk management & recovery: on average, up to 70% of defaults are recovered; long-term IRR exceeds targets despite defaults

Our Experience – Then vs. Now

Bondora used to offer high-yield categories (>25%) and speculative opportunities via the secondary market. We were excited by the returns but ultimately lost money due to high default rates and lack of guarantees. Now, Bondora has transformed into a low-risk, stable, and simple product (6% Go & Grow), with automated diversification and daily access. The high returns and speculative options are gone — as are the risks that came with them. Platform and liquidity risks remain.

Twino

Twino is a European P2P lending platform, founded in 2009 and open to retail investors since 2015. Based in Latvia, it has been regulated under MiFID II since 2021, offering stricter transparency and investor protection (segregated accounts, compensation up to €20,000).

Twino focuses on consumer loans in Poland and real estate loans in Latvia, with average returns between 10–13% for consumer loans and 4–8% for real estate. It previously operated in Russia and Vietnam but has exited those markets. The platform has a low entry threshold (from €1), a user-friendly interface, and an auto-invest feature.

Pros:

Buyback and payment guarantees reduce default risk; loans bought back after 30–60 days of delay

Diversification in loan types, from short-term consumer loans to long-term real estate projects

User-friendly platform with a clear dashboard, automatic investment tools, and mobile app

Regulated under MiFID II for extra protection

Low entry threshold from €1

Cons:

Limited liquidity: secondary market is slow; selling may take weeks or require a discount

Country-specific risk: focus on Poland and Latvia, with legacy exposure to Russia and Vietnam

Higher than average default rate (~16%), causing delays despite buyback

Cash drag: sometimes funds remain uninvested, especially with strict criteria

Stable but unremarkable returns; some alternatives offer better yields for similar risk

Withholding tax: 5% tax on interest for EU/EEA investors

Our Experience – Then and Now

In 2018, we saw Twino as a solid and accessible entry into P2P. The buyback guarantee gave confidence, but liquidity was limited, and we experienced cash drag. In 2025, this remains mostly the same: reliable and user-friendly, but with clear limitations in liquidity and geographic diversification.

Mintos

Mintos is the largest P2P platform in Europe, launched around 2015, with over 500,000 investors and more than €600 million in outstanding loans. Since 2022/2023, it’s fully regulated under Latvian and EU laws.

Mintos offers a wide range of investment options: consumer loans, business loans, mortgages, fractional bonds, ETFs, real estate loans, and ‘Smart Cash’ solutions.

Pros:

Largest P2P marketplace in Europe with 81 loan originators from 33 countries

Buyback obligation on 99% of loans after 60 days of default — provided the originator remains solvent

Broad product offering with both manual and automated investment options

Regulation and segregation: loans held in separate entities, client assets segregated

User-friendly tools and low minimum investments (€10/€50)

Cons:

Platform and lender risk: if a loan originator fails, buyback may not occur, and recovery can take years

High default rate: approx. 20.5% non-performing loans, which affects returns and liquidity

Complexity and risk: thousands of loans across many products and jurisdictions make diversification harder

Secondary market limited since 2023; new note market is growing slowly

Frequent technical issues and reported hacks

Account security: serious incidents of hacks and unauthorized withdrawals

Our Experience – Then vs. Now

Initially, we appreciated the wide variety and buyback guarantees, but the platform was less intuitive, and we encountered cash drag. Returns dropped from around 12% to 7% in 2024. In 2025, Mintos still offers a wide selection, but defaults and platform risk make the buyback less reliable. Returns hover around 10–12%, but are often reduced due to defaults.

Which P2P Platform Should You Choose?

For us personally, Robocash offers the best balance between return and convenience. Since we also have other investments that require more attention, a hands-off platform with solid returns is exactly what we’re looking for.

But every platform has its own pros and cons. The best choice for you depends on your goals, risk tolerance, and how much time you want to spend managing your investments.

Do you have any questions or want to know more about our experiences? Feel free to leave a comment!